As financial advisors, part of our job is to review our client’s financial picture from a distance, then zoom into the details that lurk in the weeds. In doing so, we often uncover areas where we can provide more value to client’s financial lives, such as savings on their income tax bill, uncovering an account with lagging performance, discovering that an account is titled incorrectly, or finding that their insurance premiums are overly expensive.

One area that we analyze under our microscope is our client’s retirement plan allocation to ensure that the asset mix is appropriate for them, and to see if we can find any areas to save on taxes now, or in the future. This analysis can get rather complex quickly, especially if we find that you have company stock in your 401K account. For example, say you work for IBM and we see IBM stock in your 401K account. If you hold employer stock in your 401K account, it may make sense to do a Net Unrealized Appreciation transaction after you retire or leave the company, in order to lower your future tax bill.

How do we perform a Net Unrealized Appreciation (NUA) transaction? First, the company stock, IBM for example, is transferred in kindto a taxable brokerage account. “In kind” means that the shares are not sold, and transfer just as they are. A very important note is that the stock cannot be transferred to an IRA account then liquidated in an NUA transaction. Second, the remaining assets in the 401K account are transferred to an individual IRA in your name. One of the rules with an NUA transaction is that the entire account balance has to be transferred out of the 401K in one year.

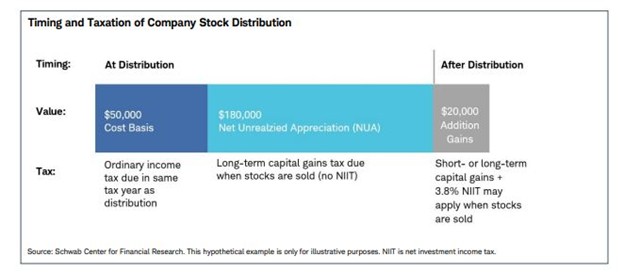

The cost basis of the shares, or what you paid for them, is taxable at your ordinary income rates in the year it is distributed in kind to this account. This portion may also be subject to a 10% penalty if the shares are sold and you are under the age of 59½.

The growth or capital appreciation (the NUA portion) above the cost basis amount is taxable at Long Term Capital Gain rates when the shares are sold someday, regardless of the holding period. The NUA portion is not subject to the 10% early withdrawal penalty once the stock is in a brokerage account.

Any appreciation above the NUA portion, however, is taxable as short-term or long-term gains, depending on how long you held the stock after it was distributed in kind from the plan.

So, why might we recommend and utilize an NUA strategy? The benefits here are that you pay Long Term Captial Gain (LTCG) tax on the stock when you sell it some day at a tax rate that is often less than what your ordinary income tax rate will be.

Also, this strategy can help to lower your future Required Minimum Distribution (RMD) amount, which is an amount that you have to distribute annually from your retirement account(s), per the IRS guidelines. The NUA transaction allows you to shift assets to a non-retirement account that does not have a required annual distribution, so the assets can grow as long as you would like them to.

Below is a graphic to illustrate a hypothetical stock allocation with a market value of $250,000 that has been transferred to a brokerage account in an NUA transaction. The tax components of the stock are then broken down by the cost basis, NUA portion, and additional growth.

If you are a bit confused by all of these acronyms, movements of shares, account types, etc. please give us a call, and we can see if a strategy like this could benefit you. Also, there are other factors that must be considered on an individual basis, which we can work through with you. That is what we are here for; everything money touches.